Machine Learning and AI for revolution of Tech Companies are changing and streamlining businesses.

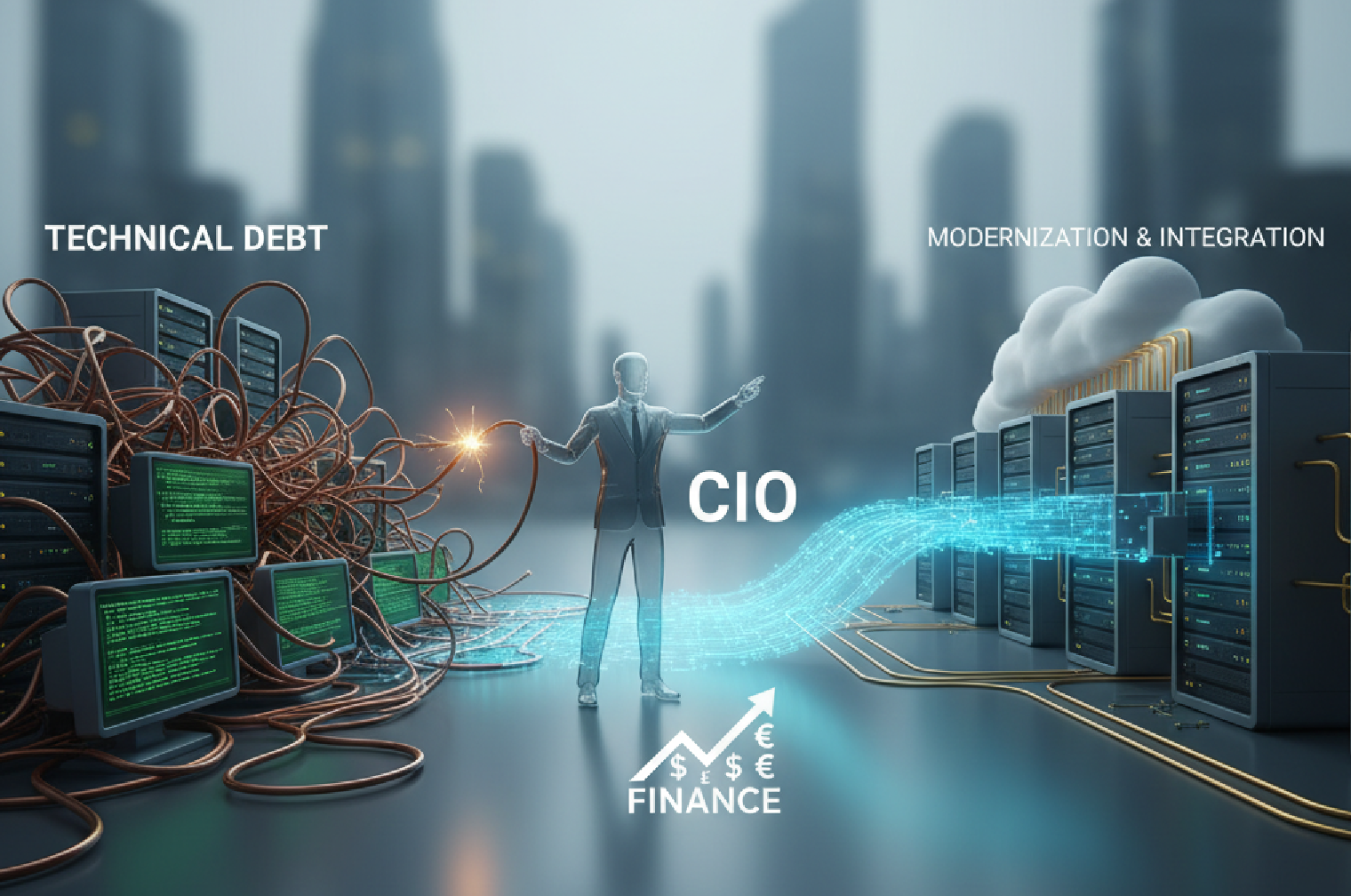

Legacy system modernization is now essential to reduce operational risk and technical debt, yet transformation must happen with near‑zero downtime in a heavily regulated, always‑on industry where service interruptions carry outsized consequences.

The fastest path forward blends progressive modernization with rigorous system integration, using API-first patterns, data interoperability, and controlled migration techniques that let core banking functions continue uninterrupted while the tech stack evolves behind the scenes.

ViitorCloud specializes in this exact balance for BFSI by designing resilient integration architectures and migration roadmaps that modernize incrementally, improve time‑to‑value, and protect business continuity from day one.

What is Legacy System Modernization in Finance?

Legacy system modernization in finance refers to updating or re‑platforming core banking and adjacent systems—often monolithic, mainframe-based, and highly customized—into modular, cloud-ready, API-driven architectures that improve agility, resilience, and regulatory responsiveness without interrupting daily operations.

Financial organizations accumulate technical debt because quick fixes, customizations, one‑off integrations, and deferred upgrades compound over years, making change risky and expensive while diverting budgets from innovation to keep‑the‑lights‑on activities.

Modernization targets those costs head‑on by progressively decoupling capabilities, rationalizing interfaces, and enabling open banking through standards-based APIs and composable services.

Read: System Integration for BFSI: Achieving Seamless Financial Operations

Modernize Legacy Systems Without Disruption

Upgrade your financial systems seamlessly with ViitorCloud’s Legacy System Modernization and System Integration solutions.

What Technical Debt Challenges Do Financial Institutions Face?

Technical debt in banking often represents a large share of the technology estate’s value, leading to spiraling maintenance costs, slower delivery, higher incident risk, and reduced capacity for new revenue initiatives, according to McKinsey’s research on tech debt’s systemic drag on transformation outcomes.

Fragmented point‑to‑point integrations, brittle batch processes, and vendor lock‑in exacerbate complexity, making core changes risky and multiplying the effort required for even routine feature releases. As a result, a disproportionate share of IT budget funds runs the bank activities, while innovation roadmaps stall under the weight of aging platforms and opaque dependencies across the stack.

Why Is Modernization a CIO Priority Now?

Bank IT spending is rising at a ~9% compound annual rate and already consumes more than 10% of revenues, making modernization essential to rein in run costs and improve ROI on digital investments, per BCG’s global banking tech analysis.

Gartner forecasts worldwide IT spending to surpass $5.7 trillion in 2025, fueled in part by AI infrastructure, meaning leaders must shift budgets from maintenance to value creation while navigating higher input costs and stakeholder scrutiny on outcomes.

Accenture notes that although banks have moved many satellite systems to the cloud, core banking remains the “elephant in the room,” so CIOs are prioritizing pragmatic, risk‑aware modernization that demonstrates incremental value and de‑risks the journey early.

How Can Banks Modernize Without Disrupting Operations?

Modernize in phases, isolating high‑change domains first and using parallel runs, feature flags, and canary releases to validate functionality in production with a controlled blast radius and clear rollback paths for safety.

Design for API-first interoperability so legacy and modern services coexist, and layer a robust integration fabric to normalize events, enforce policies, and standardize data contracts across channels and core systems, enabling reversibility and auditability at every step.

Treat observability as a migration enabler—instrument SLIs/SLOs, golden signals, and end‑to‑end tracing so anomalies are detected early and customer impact is minimized during cutovers and steady‑state operations.

- Phased migration: Prioritize “hollow‑the‑core” patterns to externalize customer, product, and pricing capabilities via APIs before moving underlying records of truth, reducing risk while accelerating visible benefits.

- API and microservices: Use domain‑aligned microservices and open banking APIs to decouple change cycles, scale independently, and integrate fintech ecosystems faster for new propositions and channels.

- AI enablement: Deploy AI for fraud detection, underwriting assistance, service automation, and incident intelligence to improve resilience and customer experience during and after modernization.

Check: System Integration in Finance: Streamlining Compliance and Risk Management

Tackle Technical Debt with Confidence

Leverage expert System Integration to modernize legacy platforms while ensuring business continuity.

Legacy vs. Modernized Banking Systems

| Dimension | Legacy (Old) | Modernized (New) |

| Architecture | Monolithic cores with tightly coupled modules that slow releases and raise incident risk | Composable, domain‑based services with API gateways and event streams for independent scaling and safer change |

| Integration | Point‑to‑point, batch-heavy interfaces that are brittle under change | API-first, event‑driven, real‑time integration that supports open banking and partner ecosystems |

| Operations | High MTTR, limited observability, heavy manual controls | Automated SRE practices, full-fidelity telemetry, policy-as-code, and faster mean time to recovery |

| Compliance | Retrofitted reporting, fragmented data lineage | Unified data models, lineage, and auditable workflows embedded in integration layers |

| Change Risk | Big-bang upgrades with major outage windows | Progressive cutovers with canary/blue‑green and rollback automation to avoid downtime |

How Does System Integration Power Finance Transformation?

System integration in finance creates a unified fabric that connects legacy cores, digital channels, risk and compliance platforms, and partner ecosystems, ensuring consistent data, policies, and SLAs while modernization occurs behind the scenes.

It standardizes API lifecycles, enforces governance, and orchestrates flows across hybrid and multi‑cloud, enabling CIOs to decouple delivery schedules and shield customers from backend change.

This discipline is the backbone for digital transformation finance programs, turning disparate systems into a coherent, resilient platform capable of continuous evolution.

Why Modernize Banking Platforms Today?

Banks that delay core and platform modernization face rising run costs, slower-than-market response, and greater operational and regulatory risk as customer expectations shift toward instant, personalized, and always‑on services.

Accenture highlights that only a fraction of bank workloads historically moved to the cloud, and value realization depends on interoperable, composable architectures—making platform modernization central to profitable digitization. With transaction banking, embedded finance, and AI‑driven risk models accelerating, modern platforms are the prerequisite for growth, resilience, and secure ecosystem participation.

Build a Future-Ready Financial Ecosystem

Transform legacy systems with modern, scalable, and integrated solutions tailored to your operations.

How ViitorCloud Supports CIOs with System Integration

ViitorCloud delivers system integration and modernization services purpose‑built for finance, unifying applications, data, and infrastructure so CIOs can execute legacy system modernization without disrupting customer experience or regulatory obligations.

From API integration and data interoperability to re‑architecture and refactoring, our teams implement domain‑specific patterns for BFSI that balance near‑term wins with long‑term architectural health and cost control.

Contact our team to set up a complimentary consulting call with our expert.

Frequently Asked Questions

It’s the process of progressively upgrading banking platforms and core systems into API‑first, cloud‑ready, and composable architectures—so capabilities evolve without interrupting daily operations or breaching regulatory SLAs.

Integration standardizes APIs, data contracts, and orchestration across channels and cores, allowing legacy and modern components to coexist safely while changes roll out in phases.

Big‑bang migrations, poor sequencing, and insufficient observability can impact customer experience and compliance; that’s why progressive cutovers, canary releases, and strong governance are essential.

Adopt “hollow‑the‑core” with targeted component exposure via APIs, migrate in phases with parallel runs, and invest in integration governance to decouple changes from customer‑facing services.

Open APIs enable interoperability with fintechs, accelerate product rollout, and decouple release cycles while supporting open banking requirements and partner channels.

Innovative tech solutions aligning with your goals

Transformation starts here

- Strategic consultation

- Collaborative approach

- Agile development